However, with the January 2021 inauguration of US President Joe Biden, the environment is very much back on the agenda. Within the first 10 days of his presidency, the democratic leader re-joined the Paris agreement and signed an extensive list of executive actions, tackling the climate crisis in the US and abroad. According to the president, a complete rewiring of the economy is now needed to avert what he calls an “existential threat” to civilisation.

Now more than ever, environmental preservation plays a more significant role in the decision-making process of investors. According to Deloitte, as of 2018, “more than US$30 trillion in funds were held in sustainable or green investments in the five major markets (…) a rise of 34 per cent in just two years”. The inauguration of this new administration has resulted in investors shifting capital increasingly towards less carbon-intensive assets. An example being the $7 trillion asset manager BlackRock making climate change central to its investment strategy for 2021. Other investors are following suit, favouring companies that are environmentally and socially conscious.

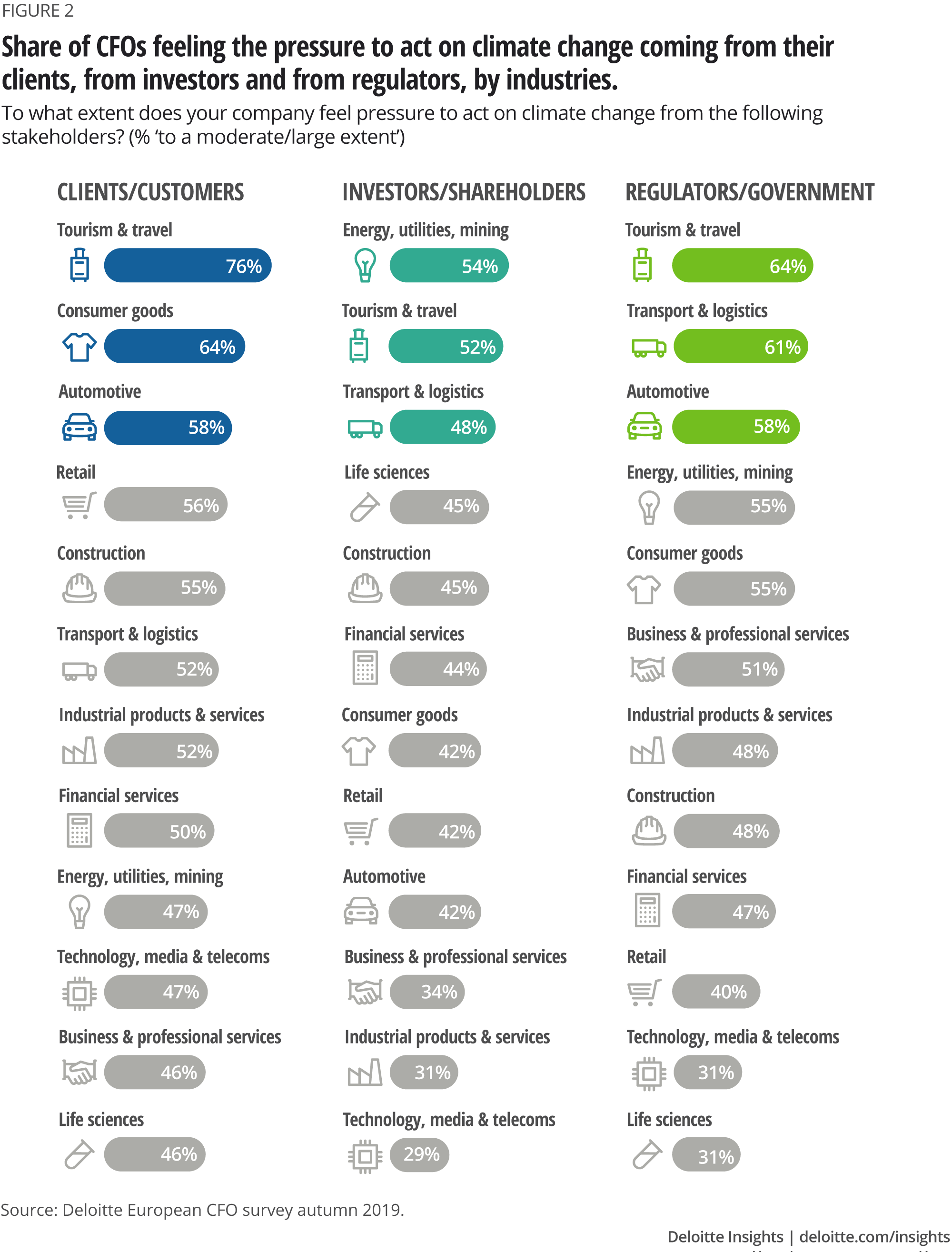

Besides the most obvious physical risks such as extreme weather and supply shortages caused by water scarcity, businesses are also exposed to transition risks which stem from a change in consumer behaviour (1). According to a 2019 Deloitte survey, financial executives in tourism and travel, consumer goods, and automotive industries are experiencing the most pressure from their clients/customers. The construction industry isn’t too far behind, sitting in fifth position. Companies are facing increasing pressure to act from a broad range of stakeholders including clients, customers, board members, management, and their own employees. As a result, social responsibility is becoming crucial for all businesses today.

The World Economic Forum states in their report “Environmental Sustainability Principles for the Real Estate Industry”, that the real estate sector consumes over 40% of global energy annually, that buildings generate 20% of global greenhouse gas emission, and use roughly 40% of raw materials. The industry is also responsible for other environmental impacts, such as waste production, pollution, water usage and consumption of other natural resources. According to The World Built Environment Forum, an initiative of RICS, key areas of focus are the reduction of energy consumption, the protection of natural resources as well as the provision of a healthy and well-being working environment (2).

To date, efforts to tackle the negative environmental impacts of the real estate industry have been more focussed on short-term cost-savings. With this as a primary focus, changes that could benefit the environment, but represent an initial cost to the business, may have been overlooked. However, integrating climate and sustainability considerations could generate financial and economic payoffs for the real estate industry in the medium and long term (3).

The World Economic Forum report states that “there are opportunities to embrace new technology and innovation to meet environmental goals and enhance business performance”. Across every sector, technology has a key role to play in sustainability and we’re increasingly seeing digital initiatives encouraging people to move away from physical and wasteful alternatives (4). However, Real Estate is usually likened to a large, slow-moving and traditional industry, oftentimes reluctant to adopt new innovations.

This is where Proptech comes in. Unissu writes that property technology companies are springing up around the world to fulfil what seems to be an ever-growing demand for social benefit and environmental impact.

ConTech is set to pick up steam in 2021 with a strong focus on tech which enables sustainable construction methods (5). Digital twins, drones, virtual and augmented reality, and robotics are amongst the latest technological innovations that have entered the construction space in the past decade. We are also seeing start-ups providing technology which is reshaping the construction industry as we know it, improving it in areas such as productivity, safety, planning, and sustainability to name a few (6) (Sophia from our US team wrote a piece about “ConTech in the time of Covid” here).

According to Qflow, data will take centre-stage in this mission. The company’s technology connects to devices on site to capture real-time environmental data, including everything from waste and materials to air quality. It feeds back the data into its cloud-based platform and uses AI to deliver key insights to the engineering team (7).

Kreo Software uses artificial intelligence (AI) to rapidly generate building design options at the concept design stage. Companies can test more environmentally friendly solutions both in terms of cost and aesthetics from day one of planning.

The scope of Smart Building is very broad, covering various objects from windows or elevators to vehicle charging. But energy efficiency is expected to mainly come from Smart Lighting (adjustment of light levels depending on time of day, sensors influencing required lighting), and smart heating, ventilation and air conditioning systems (linked to different sensors which quickly and automatically adjust to weather forecasts, occupancy, etc.) (8). Efficiency has become a synonym for sustainability, hence the terms are used almost interchangeably.

Proptech start-ups such as Berlin-based Sensorberg help by “digitising buildings” with IoT devices, mapping their energy consumption and CO2 emissions to improve those metrics. Meanwhile, German real estate service provider Apleona recently acquired a minority stake in green tech company Recogizer, which applies self-learning technology in the field of energy efficient buildings and CO2 optimisation. (9)

Check out a recent episode of our podcast ‘The Propcast: Making Workspaces Smarter’ where our Co-Founder Louisa talks to Dan Drogman and James Pellatt about the use of technology to make smart buildings which in result is making life easier.

Aspects of industry innovation, such as flexible offices, also help in the sustainability race. According to Knotel Co-Founder Edward Shenderovich, “flex is the new green”.

He explains that commercial real estate can become greener through flexible workspaces. Generally, when businesses sign traditional long-term leases, they often get too much space. As a result, they are stuck with unused space – a major drain on resources – which still needs to be maintained with lighting, heating, cooling and other energy-consuming features. Businesses choosing to relocate also results in a time-consuming process with a steep environmental impact. Around 100 billion cardboard boxes are used each year in the U.S., and a significant proportion of this sum is the result of relocations. This cycle produces 850 million tons of cardboard waste annually (10). “[A] flexible approach helps eliminate grey space, reduces the total resources businesses burn through, and cuts down on relocation waste. It’s a win-win for enterprises and the environment”, Edward concludes.

According to the 2020 Global Status Report for Buildings and Constructions, the “elimination of building emissions by 2050 is possible with existing technologies”. Being in the European team at LMRE, I have been seeing many start-ups leveraging technology to focus their activities on environmental issues. They promote a circular economy to create new innovations which not only aim to mitigate the effects of climate change, but also proactively find solutions to fight against it. I look forward to strengthening my knowledge on the subject and exchanging with these companies in the future.

LMRE are specialist PropTech recruiters, if you need help growing your business or making any key hires please get in touch via the form below!

"*" indicates required fields

{kind=link}